Why October/November Is the Time to Act

Every year around this time, I get the same kind of call.

A client rings me in October (usually late October) and says something like:

“I just found out I can still get tax relief for last year — can I do anything before the deadline?”

The answer, of course, is yes. And it’s one of the simplest ways to save money while also saving for your future.

October/November is the one window where you can make a pension contribution and backdate the tax relief against your 2024 income. Miss it, and that opportunity is gone for good.

Why This Matters

- Immediate benefit: You’re not just saving for retirement, you’re also reducing this year’s tax bill (or even triggering a refund).

- Future benefit: You’re moving money from your current account into your long-term wealth and getting the government to boost it along the way.

- Peace of mind: Instead of letting another year slip by, you’re actively building towards the retirement lifestyle you want.

How Pension Tax Relief Works

When you contribute to a pension, the government gives you tax relief at your marginal rate:

- 20% for standard-rate taxpayers

- 40% for higher-rate taxpayers

So a €1,000 contribution effectively costs:

- €800 at the 20% rate

- €600 at the 40% rate

You’re essentially moving money from Revenue’s pocket into your retirement plan.

How Much Can You Contribute?

Revenue sets limits based on your age, as a percentage of your earnings (capped at €115,000):

| Age | Max % of Earnings |

|---|---|

| Under 30 | 15% |

| 30–39 | 20% |

| 40–49 | 25% |

| 50–54 | 30% |

| 55–59 | 35% |

| 60+ | 40% |

How it works?

🔹 Emma (35, earning €40,000)

- Contribution limit: 20% = €8,000

- Tax relief: 20% = €1,600

- Net cost = €6,400 while €8,000 goes into her pension.

🔹 Mark (42, earning €120,000)

- Contribution limit: 25% of €115,000 (cap) = €28,750

- Tax relief: 40% = €11,500

- Net cost = €17,250 while €28,750 goes into his pension.

For both Emma and Mark, the tax system is designed to reward them for saving but only if they act before the deadline.

How to Claim Relief (Step by Step)

Making the contribution is half the job — you also need to claim the tax relief. Here’s how:

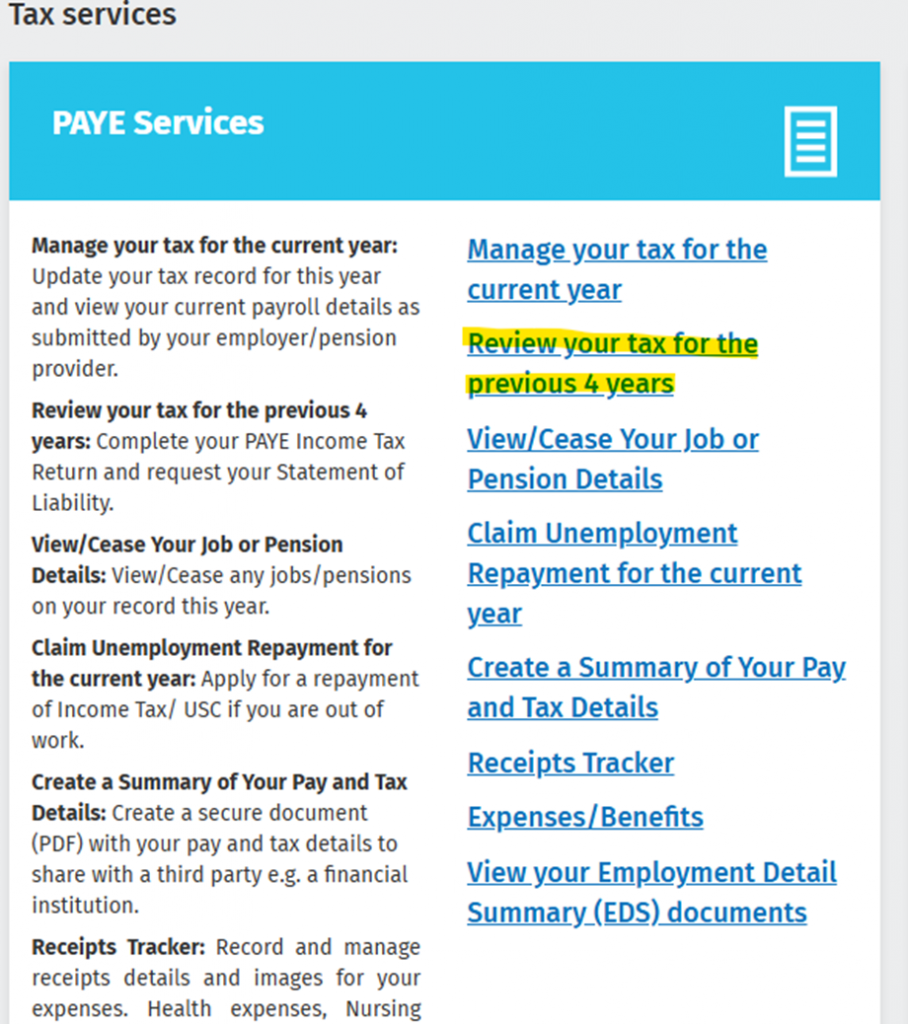

Step 1. Log in to Revenue.ie → MyAccount.

Step 2. Under PAYE Services, click Review your tax for the previous 4 years.

Step 3. Select the relevant year (usually the previous year).

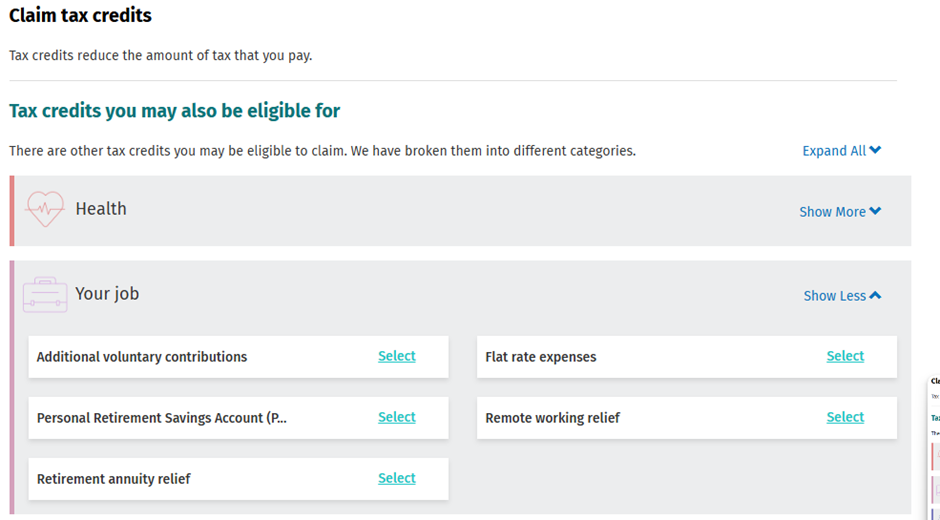

Step 4. Under the “Your Job” section, choose the correct option:

- Additional Voluntary Contributions (AVCs)

- PRSA contributions

- Retirement Annuity Relief (personal pension)

You’ll be asked for contribution details and to upload supporting documentation (your provider/advisor can supply this).

Step 5. Review and submit. 🎉

You’ve just reduced your tax bill and maybe unlocked a refund.

My Take

I’ve seen the difference these October/November contributions can make. For some, it’s a welcome refund landing just before Christmas. For others, it’s knowing they’ve finally taken control of their retirement planning.

The key is: don’t leave it too late. Once the deadline passes, you can’t go back and claim for 2024.

The Bottom Line

If you’ve got money sitting in your bank account, ask yourself:

👉 Would you rather leave it there earning next to nothing or move it into your pension, grow your future wealth, and get 20–40% of it straight back through tax relief?

This deadline comes once a year. Don’t miss it.

📌 If you’re not sure how much you can contribute or how to claim the relief, I’ll help you run the numbers and walk you through the Revenue process. Book a quick call and we’ll get it sorted before the cut-off.